Beneath the Ceiling, Above the Bias: Why Africa Deserves Better from the Realm of Ratings

Because not all "Junk" is created equally.

Reporting in the Sunday Times last week about the “Call for Change in the Way Credit Ratings Agencies Deal with Africa” from the Afreximbank 2025 AGM in Abuja got me thinking. From there I did some reading, and so here is what I have learnt.

African countries face a severe infrastructure financing gap of about $130 - 170 billion needed per year versus a shortfall of about $100 billion. What may be a key barrier is that sovereign credit ratings on the Continent remain overwhelmingly in the “junk” category. I’ve come across many African leaders (in Government and in Business) and analysts who argue that this doesn’t just reflect the fundamentals but outdated assumptions and biases in ratings methodologies. Professor Jeffrey Sachs (US Economists) goes further and says they use “crude, cookie cutter” methodologies based on “useless indicators”. Having read the article in the Sunday Times (Business Times) this past weekend, I wanted to examine those outdated assumptions, and how they hurt development. I was particularly interested in the Sovereign Ceiling rule. I hope to also recommend reforms that could lower borrowing costs, unlock infrastructure finance and boost socio-economic growth.

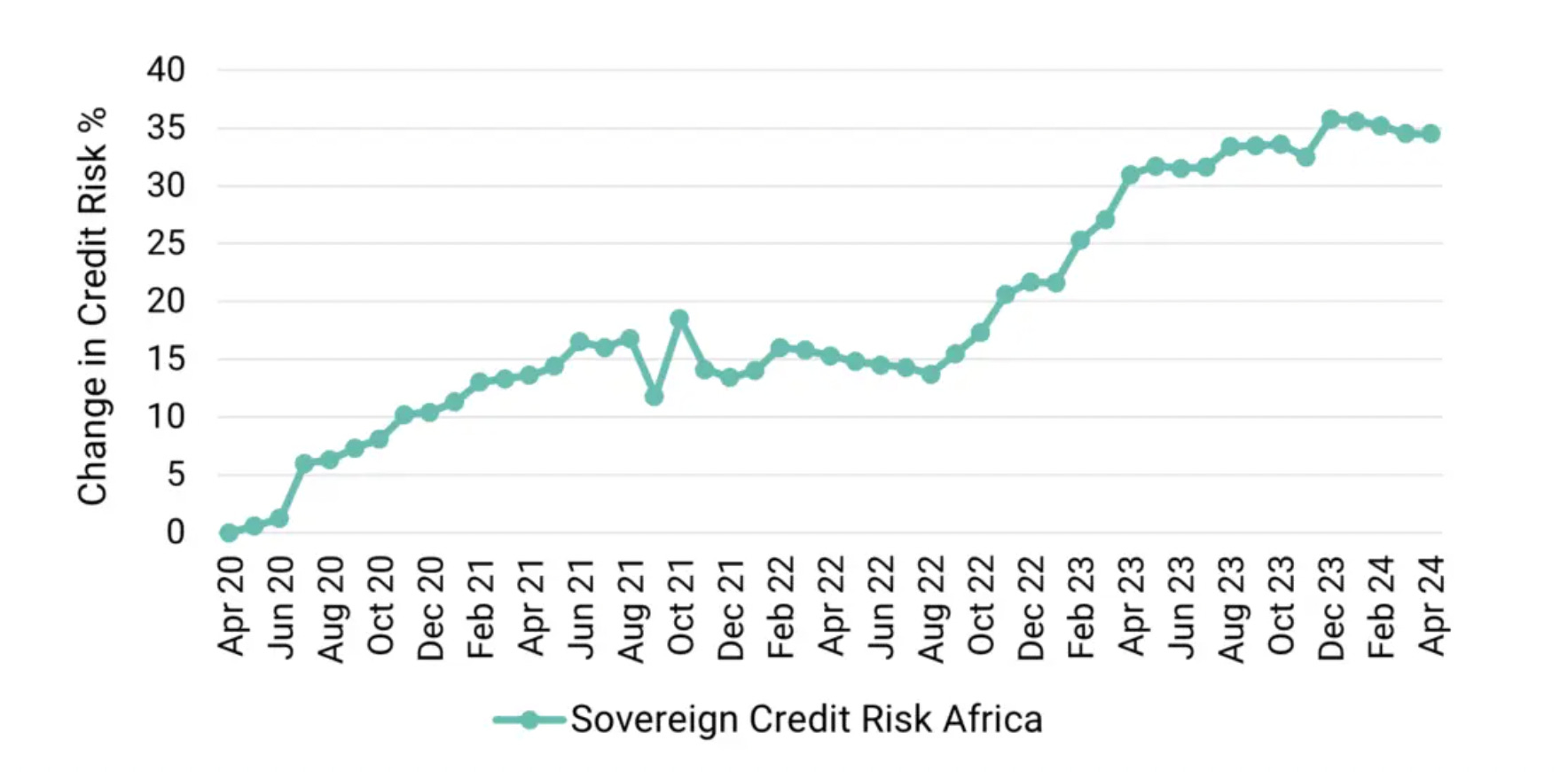

Source: Credit Spotlight on African Sovereign Ratings (Carruthers, 2024).

Credit rating agencies (CRAs) typically use global, formulaic models to judge risk, but these often fail to capture Africa’s diversity and progress. A common assumption is that African economies are inherently high-risk (e.g. due to governance issues, weak institutions or commodity dependence) regardless of recent improvements. In practice, this leads to many African ratings being “pessimistic.” Here’s a recent instance of this: During the COVID-19 shock almost all African sovereigns were downgraded, even those with only moderate deficits, prompting complaints that agencies “overreacted” and reinforced an implicit “Africa risk premium”. Likewise, agencies may give very little weight to recent reforms. After countries like Ghana or Nigeria took steps to improve debt transparency or fiscal policy, CRAs have been slow to upgrade their ratings, at least by my estimation. A study I happened to come across noted the underrating of African countries compared to quantitative models implying that subjective judgements (perhaps driven by caution or limited on-the-ground insight) play too large a role.

African critics also highlight flaws in the variables that CRAs use. I’m not nearly smart enough to be sure, but examples are made of major agencies penalising countries for export concentration or recent debt relief factors that disproportionately affect African states. A review of CRA methodologies observed that increases in international interest rates and narrow export structures count against ratings, meaning that by design, African countries are at a disadvantage after debt relief. In practice, countries that diversify or build long-term resilience may see no credit benefit. The NTU Centre notes that incumbents “often fail to account for the long-term economic benefits of climate-related investments,” even if those projects strengthen future growth. Agencies focus on short-term fiscal metrics while ignoring sustainability and development gains. In short, the outdated assumptions include; excessive risk aversion, neglect of reform efforts, an over-reliance on stale data or proxy indicators and a one size fits all methodology (ignoring diaspora remittances, informal markets, etc).

Source: Credit Spotlight on African Sovereign Ratings (Carruthers, 2024).

One long-standing policy of CRAs is the “sovereign ceiling”. No borrower in a country can get a higher credit rating than the government itself. Why not? In practice, this means most African corporates or sub-national projects are capped by the already low sovereign score. It seems to me a lazy way to reflect country risk, and as critics have noted, it unduly restricts private sector credit. A well managed power company in Kenya, or a mine in Botswana, may have steadier cashflows and foreign earnings that would merit a higher rating but they remains tethered to the sovereign.

Reforming or softening the sovereign ceiling would better serve African development. For example, the use of credit enhancements can effectively lift a project above the ceiling. A multilateral bank might provide a partial guarantee for an infrastructure bond. Such a guarantee could raise the bond’s rating above the sovereign level, attracting institutional investors who require higher-grade debt. Expanding these tools is one practical reform I have come across, and there are many others. Over time, regulators could also allow fully domestic companies or projects with independent revenue streams to be rated on their own merits, rather than strictly capped by a sovereign ceiling. This may, unofficially, be happening already but if it is why should it not be official?

There are plenty more reform ideas out there and I have chosen a few of my favourites. While the African Union has initiated the African Credit Rating Agency (AfCRA) to provide “fair, transparent and development-focused” ratings for African economies, countries on the continent can earn better scores by strengthening fundamentals - no matter the rater. Key reforms include prudent fiscal and debt management, economic diversification, and better institutions. Secondly, African government should maintain an open dialogue with ratings analysts. Inviting agency representatives on fact-finding missions, sharing policy roadmaps, and promptly clarifying any “misconceptions” can lead to more accurate ratings. Local Multilateral Development Banks can play a larger role by stretching their balance sheets further for strategic African projects, by guaranteeing bonds and using blended finance, while supporting sovereigns to build capacity. Penultimately, I can’t imagine it would hurt for regulators to instruct CRAs to apply more flexibility when it comes to the Sovereign Ceiling principle, if they won’t do away with it altogether. For instance, if a project’s revenues are fully secured by hard currency contracts or by an international off-taker, agencies might rate it above the sovereign. It isn’t a practice that is unheard of in non-African markets. Lastly, methodologies need to be modernised to include metrics on climate risk/opportunity, social development investments, or institutional reforms tied to sustainable development objectives. If we explicitly recognise that infrastructure linked to clean energy, water, or health boosts long-term resilience, African governments could allocate more resources to strategic spending in these areas rather than see ratings penalise them.

Reforming rating practices is not just an academic issue, it has concrete implications for development. Lower borrowing costs and greater market access can dramatically boost sustainable infrastructure and social programs. For example, President Ruto cited research that a one-notch rise in Africa’s average sovereign rating could unlock about $15.5 billion in extra funding – enough to cover roughly 80% of the continent’s infrastructure needs. To put that into perspective, improved ratings could mobilise more capital than all official development aid combined.

African Credit Rating Agency to Launch by September 2025

credit rating reforms in Africa have real policy weight. A more balanced and context-aware ratings framework would reduce borrowing costs, freeing billions for roads, power and schools. It would help attract private capital for sustainable projects and accelerate African development. By advocating these reforms – from supporting an African-led agency to rethinking the sovereign ceiling – leaders can ensure that African economies are assessed more fairly. This, in turn, would unlock the investment needed for a more prosperous and resilient future on the continent.